Abstract

This essay provides an analytical description of the great recession of 2007-2009. With an emphasis on the USA, this paper tries to explore the underlying causes of the recession and the consequences of the financial crisis and the credit crunch. This paper also deals with the policy actions taken to mitigate the effects by the US government and the Fed. Monetary policy measures were considered in detail and last but not least IS-LM framework was used as supporting evidence to discuss the effectiveness of the monetary policies. The paper is also backed up by considerable empirical evidence gathered from research papers and free government/world bank databases.

Keywords: Crisis, IS-LM framework, Credit Crunch, Recession, Monetary policy, fiscal stimulus, CDO, mortgage.

Introduction and Overview

After the boom years of 2002-07 the world economy especially the United States, the United Kingdom, and the rest of European economies, faced a catastrophic turnaround and they faced a recession during the years 2007-09 as 2009 became the first year since the second world war when the world was in recession (Islam, 2010).

The effect of the global financial crisis or the great recession whatever we may call it lead towards the huge economic downturn from the last quarter of 2007 to the third quarter of 2009 in the United States (Christiano, 2017).

The economic crisis which had its impact on the activities of largely every country and region emanated from the credit markets in the USA and other developed countries. As a result of it, the atmosphere of easy credit conditions transformed into a situation of ‘credit crunch’ (situation of tight credit conditions), and in some cases, it had also lead to dysfunctional markets.

The global financial crisis of 2008 lead towards the decline of confidence in individual consumers and business entities leading to a significant impact on the global activity. There was already this large run-up in housing construction and dwelling prices in response to the rising policy rates during the mid of the year 2006 which had a dampening impact on the economy of the United States. In the background of extreme uncertainty, the households reduced their consumption and the demand for manufactured goods. All of these events lead towards an extraordinary fall in industrial production worldwide by the end of the year 2008 and the GDP of the US along with other major economies contracted (Edey, 2009).

Causes

To overcome the recession in 2001, US monetary authorities kept on reducing the policy rates to unusually low levels. This helped to overcome the 2001 recession and ensured that it is short-lived but the resulting boom in the economy was largely due to the debt-financed consumption which had managed to increase the aggregate demand globally set the stage for the impending recession of 2009-09 (Islam, 2010).

Astley et al (2009) as cited in Islam (2010), held the US housing market as the force that triggered the Great Recession. The delinquency of credits which had started during the year 2006 gained momentum when the US Federal Reserve started to increase the interest rates. With larger and larger delinquencies and the rise of bad loans, many mortgage lenders declared bankruptcy and failed. The sub-prime market uncoiled. One of the most serious implications of the complex financial products such as CDOs and credit default swaps, many financial institutions did not have any idea about the size of losses. As a result, the institutions started hoarding liquidity leading towards the freezing of the market for asset-backed commercial papers. The resultant credit crunch resulted in the increased perceptions of risk and shortfall in lending. However, the collapse of the investment bank Lehman Brothers led to a fall in the financial system in September 2008.

Due to the expected increase in the interest rate, customers felt the inability to repay the loans and in order to get some additional gain decided to sell their house. Banks in order to cover the loan risks also increased the interest rates from 3% to 5%. And when the borrowers tried to sell their houses, the increased interest rates had caused the scarcity of potential customers and since they did not find the buyers the housing prices started to fall, and bubble burst. This lead to the borrowers defaulting on the loans and banks faced to empty houses. All these chronologies of events started the chain reaction of bank failures one after another and the global recession started (Azar; Mansouri, 2011).

Many economists as mentioned by Christiano (2017) believe that the financial crisis was caused by a mix of declining house prices, shadow banking system, heavy investment of the financial system in house-related assets coupled with the interlinking of factors such as loose monetary policy, global imbalances, lax financial regulation along with the misperception of risks (Islam, 2010) lead to this financial crisis of 2008.

All these factors also led to a reduction in household wealth following the credit crunch and declining purchase of houses with a fall in the housing prices. Households cut back on spending. This caused the sales to decline substantially and the firms pull back on investment and hiring. All these factors reinforced one another and horned the economy into the tailspin of recession (Christiano, 2017).

Consequences

Of all the other consequences, the great recession also had a disproportionately large impact on the discipline of macroeconomics, and economists were forced to reconsider the discarded theories such as the IS-LM framework, etc. The damage which the national economies had top face is yet to recover. There was a severe impact on macroeconomic variables such as consumption, employment, investment, output, etc. The drop in the magnitude of these variables was larger than the average of all the recessions since 1945. The decline in Employment, for example, was 6.7% and for consumption and output, it was 5.4% and 7.2% respectively (Christiano, 2017).

A global job crisis also emerged from the global financial crisis as the tightening credit conditions damaged the real economy and the trades collapsed. Unemployment increased like anything and millions were impoverished. The United States economy as the USA was at the epicenter of the crisis was hit severely. The US economy after falling into the recession shrunk by 2.7% by the year 2009 and largely these repercussions were the results of the financial crisis and the credit crunch. In the USA due to the fall in prices, there was an increase in the real wage. The falling prices also led to an increase in real hourly earnings. Interestingly the great recession had contributed to the correction of the previously deteriorating real hourly wages which were fueled by the rising inflation and constant nominal wages before the financial crisis of 2008-09 (Islam, 2010).

An average household in the USA lost nearly $5,800 of income as a consequence of the lowered economic growth. On the other hand, the Fed spent $2,050 on average, for each household to alleviate the effects of the financial crisis. The total loss summed up to about $100,000 per household due to the combined effects of the fall in house prices and the prices of the stock during the periods of the great recession between July 2008 to March 2009 (Swagel, n.d.).

Policy Response

The policy response to the crisis incurred gigantic costs to the US government as the public debt was already high due to the low levels of revenues and high levels of the spending to mitigate the impacts of the crisis (Swagel, n.d.).

In the United States, noticeable measures were taken to remove the bad assets from the balance sheet of affected financial corporations and to purchase the long term securities for supporting the mortgage and the private credit markets (Edley, 2009).

We can therefore conclusively group the US policy response into two broad categories:

Measures to target the immediate issues of reconstructing the damaged credit markets and regain the demand and other economic activities.

Measures directed to reduce the risk of occurrence of a similar crisis in the future.

According to the works of Azar and Mansouri (2011), the governments tried to inject massive amounts of credit into the financial markets. They also went for nationalizing the banks, lowered the interest rates, and increased discretionary spending by the means of fiscal stimulus packages. Thus, we can categories the policy response in the view of the great recession in the following categories:

For keeping the credit flowing the devised bailouts to inject money into the financial systems.

To deal with the credit crunch they slashed down the interest rates. Thus stimulating the borrowings and investment.

There was a fiscal stimulus to increase aggregate demand.

Monetary Policy Response And Its Impact

Initially, in the wake of the housing market collapse in 2007, the Federal Reserve System continued to increase the supply of money and kept on lowering the interest rate. This managed to keep the economy afloat until the end of the year 2008. Then arrived the major problem that the interest rates were already reduced to zero and the collapse of the US housing market had caused a serious negative impact on the financial system. And since the money supply could not have been increased by way of reducing the interest rates, various monetary and fiscal actions were taken. The monetary policy actions taken to stimulate the expenditure can be discussed as follows (Sims, 2003)

Quantitative easing- Longer maturity rates, priced according to the safer longer terms assets (private sector debt with longer maturities, treasury bills, and bonds) such as mortgages are relevant for the firms and the consumers. And normally the monetary authorities try to affect the short term interest rates which then through a standard term structure manages to affect (lower) the longer rates. By this policy of quantitative easing, the Fed bought the longer-term assets as an attempt to directly lowering the longer-term interest rates.

Operation Twist- This was one of the non- standard policy of the Fed, where in order to lower the long rates, the central bank bought the bonds of longer maturity and sold the bonds of shorter maturity.

Forward Guidance- Fed, announced explicitly its intentions regarding the promise of lower short interest rates in the future in order to reduce the longer maturity rates in the present.

The simple understanding of these policies is that they are intended to avoid the deflation and deflationary expectations trap. The three policy majors signaled implicitly higher future inflation levels. The Fed effectively promised to bring in future expansionary monetary policy trying to raise the inflation levels. Thus, the current expected levels of inflation may also rise if people anticipate this future expansionary monetary policy. And this can stimulate investment and consumption levels provided that the nominal interest rates are already close to zero. This can be depicted by a downward/rightward shift of the LM curve as we will see next.

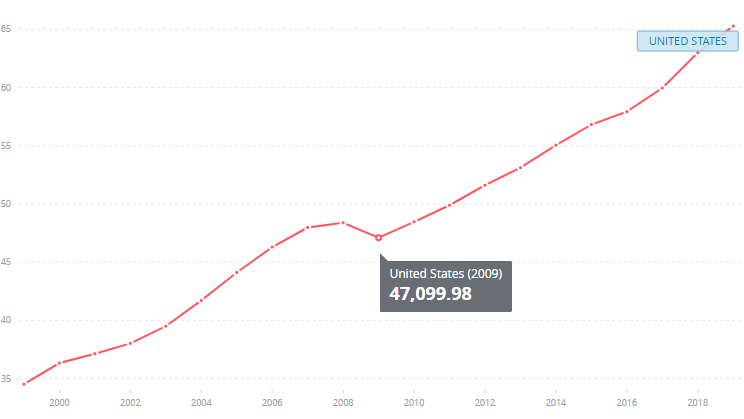

Now let us look at the plot of real GDP per capita of the US and we can comment on the effectiveness of the policy actions.

Source: The World Bank Data. Retrieved from https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?end=2019&locations=US&start=1999

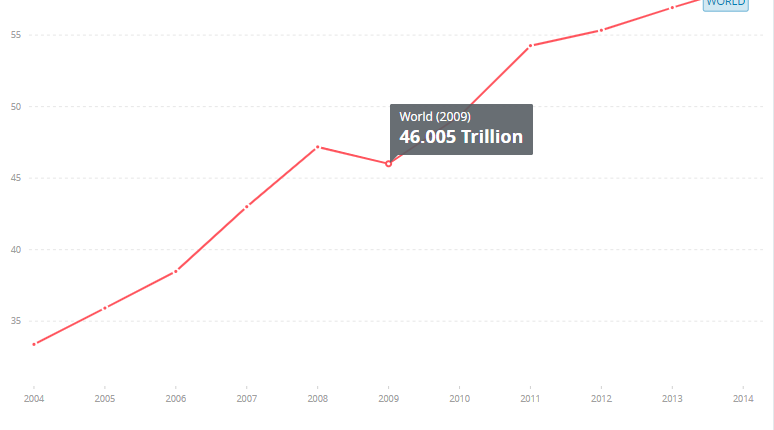

We can also analyze the data for consumption expenditure over the periods of the great recession and observe the changes in them to comment on the effectiveness of the policy decisions.

Source: The World Bank Data. Retrieved from

https://data.worldbank.org/indicator/NE.CON.TOTL.CD?end=2014&start=2004

IS-LM Framework As Supporting Evidence

The great recession can be characterized by the negative shock to the demand for goods. This is going hand in hand with the traditional macroeconomic model captured by Hicks and Hansen in their IS-LM model (Christiano, 2017). Thus we can use this model to explore the underlying conditions about the US economy and evaluate the policy responses.

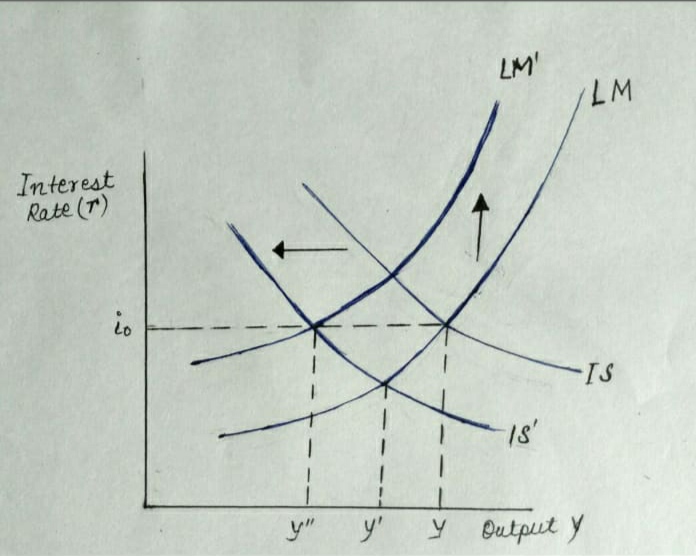

According to the works of Swain (2009) as cited in Azar and Mansouri (2011), due to the fall in personal consumption in the US, the IS curve shifted leftward. This led to the decline of the output as shown in the figure below to Y’. In order to maintain the target interest rates, there was an upward shift of the LM curve decreasing the output further to y”.

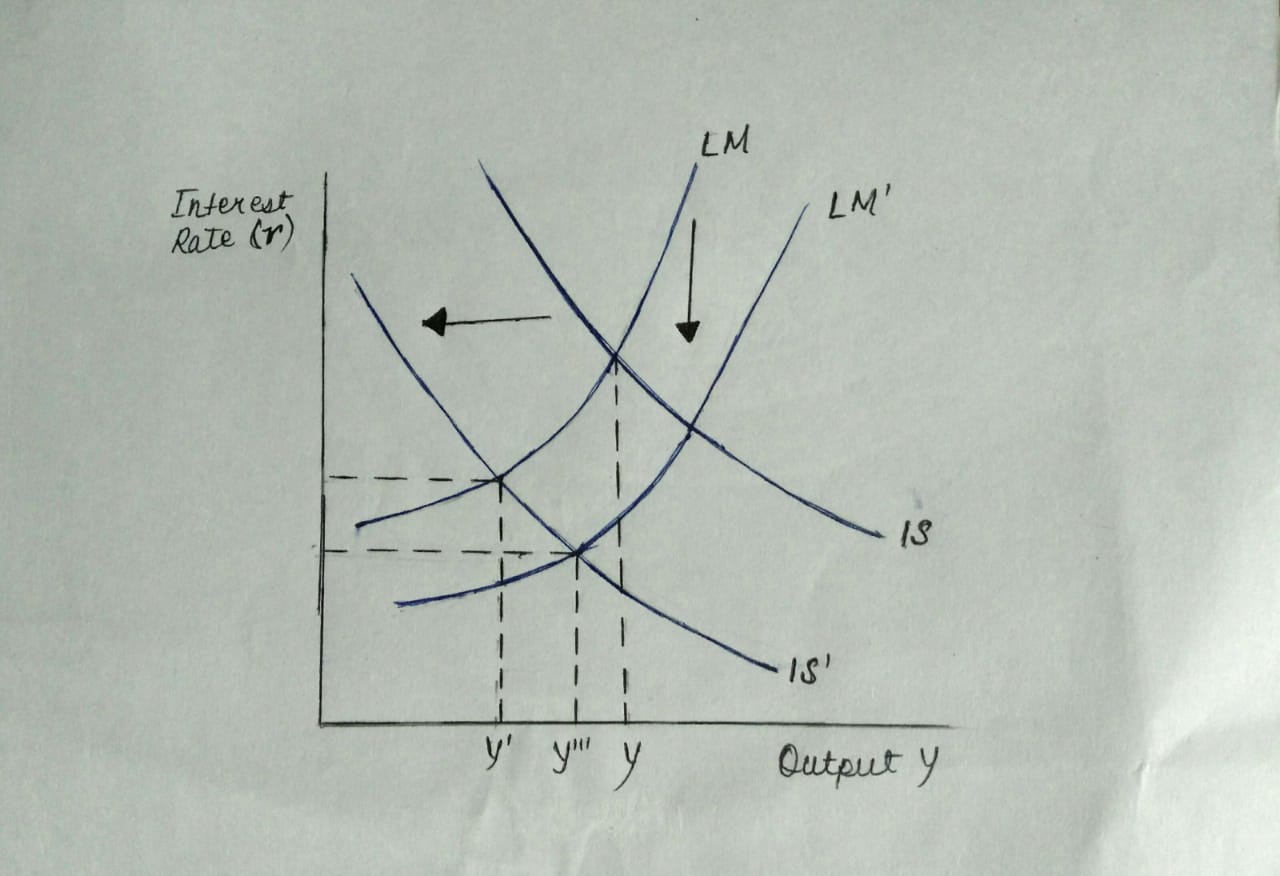

Now the Fed cut and dramatically reduced the policy interest rates. This increased the liquidity in the cash market leading towards a downward shift of the LM curve. This will offset the effect created by the leftward shift of the IS curve, attempting to maintain the output levels to y’” in the short run as indicated by the graph below. The real interest rate declines with the consumption and investment both increasing.

Conclusion

Despite all the measures the US economy took over five years to return to the 2007 level of output per capita. Empirical evidence (Christiano, 2017) suggests that the United States is still below the trend growth in 2007 by about 10%. The work also highlights that the need of the hour is to try and reduce the onset and severity of any such future crisis and global recessions.

The great recession also showed us the relevance of developing new economic theories, especially in the financial sector. Study and research in the field of international finance and economics are also very important as when a great economy like the USA faces a crisis, it becomes the global crisis.

References

Edey, M. (2009, September). The Global Financial Crisis and its Effects. Retrieved August 02, 2020, from https://onlinelibrary.wiley.com/doi/epdf/10.1111/j.1759-3441.2009.00032.x

Golmohammadpoor Azar, K. (1970, January 01). 2008 Economic Crisis Analysis: The Macroeconomic Approach. Retrieved August 02, 2020, from https://www.econstor.eu/handle/10419/49648

The Great Recession: A Macroeconomic Earthquake. (n.d.). Retrieved August 02, 2020, from https://www.minneapolisfed.org/article/2017/the-great-recession-a-macroeconomic-earthquake

Sims, E. (2013). Intermediate Macroeconomics: Great Recession. Retrieved from https://www3.nd.edu/~esims1/great_recession_fall_2013.pdf

Swagel, P. (n.d.). The Cost of the Financial Crisis: The Impact of the September 2008 Economic Collapse. Retrieved from https://www.pewtrusts.org/-/media/assets/2010/04/28/costofthecrisisfinal.pdf

Verick, S., & Islam, I. (2010, May). The Great Recession of 2008-2009: Causes, Consequences and Policy Responses. Retrieved from http://ftp.iza.org/dp4934.pdf

A very well written and detailed analysis of the great recession. Good job!!

ReplyDeleteWow. Indeed wonderful. The way it has been explained by you is fantastic. Neat graphs. The best part about this is that it can be understood by a layman as well. The formatting is great as well.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteReally informative and well explained!

ReplyDeleteVery well written ! Good job !

ReplyDeleteThe level of research is quite visible. Can't expect anything less from you. Keep up the good work.

ReplyDeleteReally informative stuff

ReplyDeleteWell presented and lucid explanation!!

ReplyDeleteVery Informative and well structured! Great work.

ReplyDeleteThe author not only understands his stuff well but also knows how to present it to his audience in a nice way!Good job!

ReplyDeleteA well structured write-up on the recession in America! Great job bro!

ReplyDeleteWell analysed write up! Good insights

ReplyDeleteIncisive Piece!

ReplyDeleteVery well articulated point. Keep it up!!

ReplyDeleteVery well written!

ReplyDeleteWell researched and written! Good job

ReplyDeleteVery informative, systematically presented. US housing market was the epicenter of this global crisis. Insights provided are comprehensive.

ReplyDeleteA detailed and reader friendly analysis. Good job...

ReplyDeleteGreat work, amount of effort put in is clearly visible.

ReplyDeleteGood observation. Keep it up

ReplyDeleteVery informative, I couldn't stop myself from reading once I started.Really looking forward to more

ReplyDeleteNicely written, informative keep going

ReplyDeleteVery well written!! So informative!!

ReplyDeleteVery informative

ReplyDeleteVery well written

ReplyDeleteVery well explained with logical sequence of actions.

ReplyDeleteAwesome explanation using the IS - LM Curves. Nice analysis!!

ReplyDeletevery well articulated and written!

ReplyDelete